How we spent just $18 for two Business Class seats to our Honeymoon in Southeast Asia.

We spent $18 USD for not one, but TWO business class seats from Chicago, Illinois to Bangkok, Thailand for our honeymoon. Imagine stepping onto your honeymoon flight, turning left towards the front of the plane, you and your new spouse are offered glasses of champagne as you settle into your lay-flat seats on a 18 hour flight to your romantic honeymoon in Thailand, Indonesia, and The Philippines.

Now picture the utter glee in knowing you paid a little more than the quick airport Starbucks breakfast for these seats.

Welcome to the magic of The Points Plan where we map out a plan to leverage your everyday spending to earn points and miles and score flights like this!

Sound too good to be true?

Here’s our receipt!

We firmly believe that only spending $18 on your honeymoon flight is a love language.

How did you pull this off?

We leveraged our wedding expenses and turned them into points and miles.

Weddings are EXPENSIVE. The venue, flowers, catering, the dress, the tux, invitations, the list goes on and on.

We came up with a plan:

We (responsibly!) openend the right travel rewards credit cards.

Earned their Welcome Bonuses by systematically putting all of our available wedding expenses on those credit cards.

ALWAYS paid the entire credit card statement balance on time, every month. Never carry a balance.

No, you can’t just put everything on an airline credit card that you’ve had for years.

Let’s break this down.

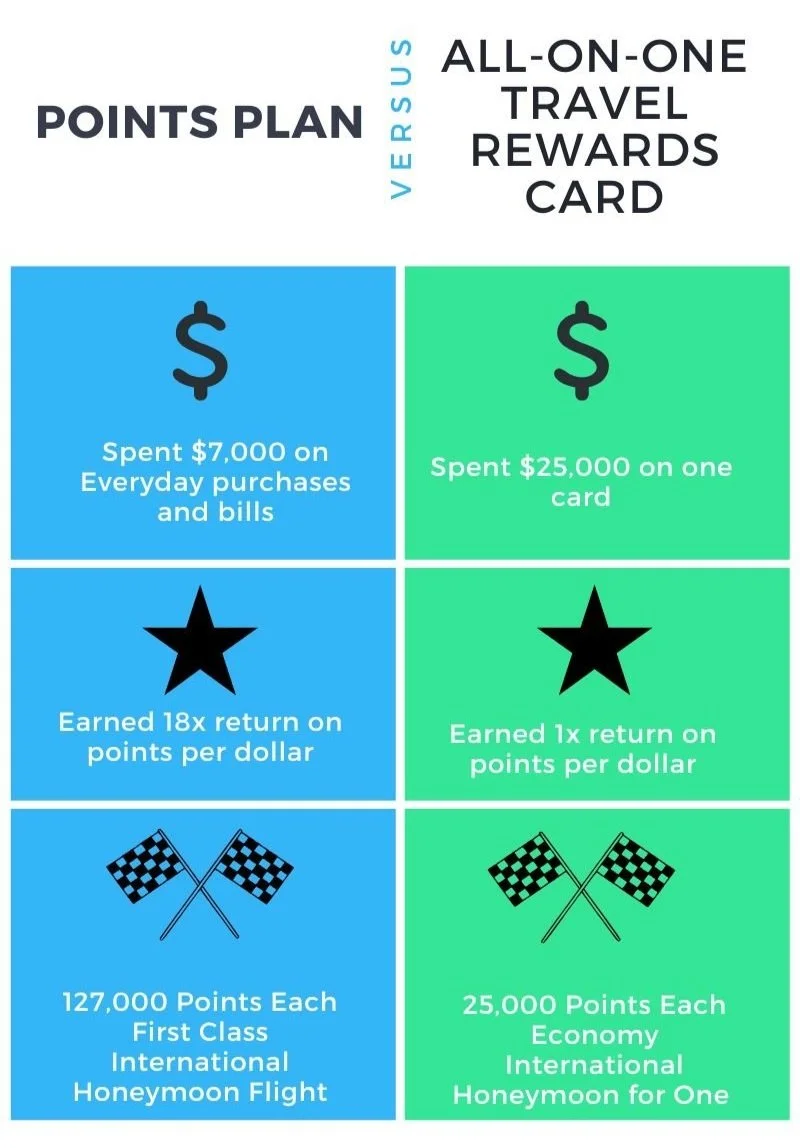

You’ve had the same travel rewards credit card or airline credit card for years, and have been dutifully spending on that credit card to rack up the points or miles. Great!

Here’s the kicker. Most travel rewards credit cards earn just 1 point or mile per $1 spent. That means you’d have to spend $25,000 to earn 25,000 points. Ouch.

With a Points Plan, we find the deals that offer a huge Welcome Bonus; something like earn 75,000 points after spending $4,000 in the first 3 months of your credit card opening. Stay with me here.

That means you’re earning 18 points/ miles per dollar spent, not 1 for the first $4,000.

Bottom line, you would earn 75,000 points instead of 4,000 points for the same money spent on your credit card.

Opening a new credit card will NOT hurt your credit score.

Let’s take a minute to de-mystify credit scores:

And no, checking your credit score will also NOT hurt your credit score.

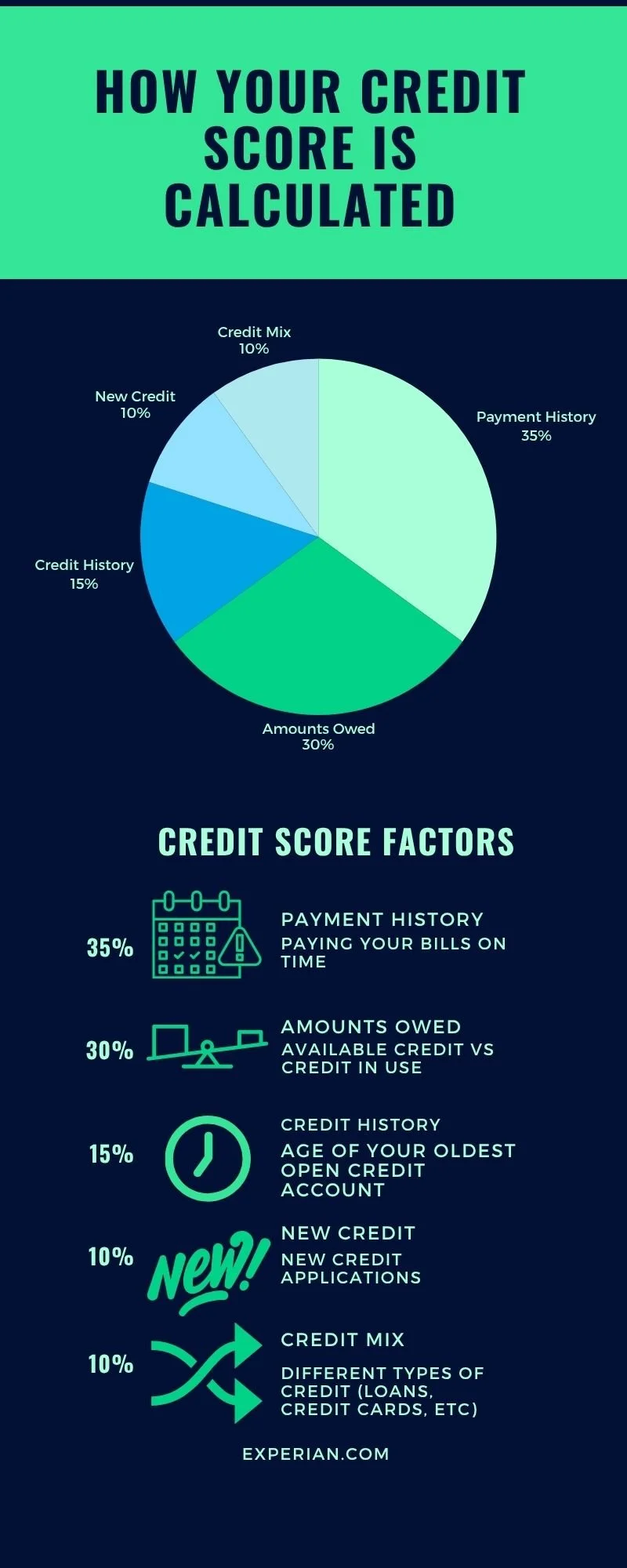

Your credit score is calculated based on 5 different metrics.

Payment History: Your history of paying your bills on time and in full.

Credit Utilization: This is a ratio of how much your allowed to borrow versus how much you actually borrow. For example, your credit card allowance, vs how much you actually spend each month.

Credit History: How old is your credit history? Your oldest loan or credit card?

New Credit: How many recent credit applications? This is the part where you don’t take out a new car loan when buying a new house.

Credit Mix: What types of credit do you have? Car loan, student loans, mortgage, credit cards, etc.

Now, what does opening a new credit card actually do to your credit score:

When opening a new credit card, the issuing bank will do what’s called a “hard inquiry”, meaning they will pull your credit score to review these factors.

Your credit score will take a tiny hit when a hard inquiry is pulled, which usually resolves itself within a couple of months

Over time, your credit score actually improves because:

Payment History Improves: continue paying your new credit card on time and in full.

Credit Utilization Improves: more available credit, but again, not maxing your new credit card out.

Credit Mix Improves: A new line of credit improves your credit mix.